- Thursday, 21 May 2026

Make Revenue Collection Rights Clear

Nepal’s constitution has divided the state power between the state units - federal, province and local level. There is no denying that optimum amount of revenue mobilisation in sub-national governments (SNGs) is essential for the success of federalism. So, the constitution calls for the equitable distribution of revenues between three levels of governments since commensurate revenue with the economic functions will facilitate to fulfil the constitutional responsibilities of each level of government. A meaningful level of own source revenue enables SNGs to be responsive to local needs and exercise a high level of discretion in delivering services and undertaking development activities.

To serve this objective, the constitution has arranged general lists of revenue assignment (schedules 5, 6, 8 and 9) and related legislations have elaborated the independent, common and concurrent revenue functions of the federal and SNGs. The constitution gives the federal government, to some extent the province too, a role in shaping the revenue framework of the local government. Local Government Operation Act 2074 and finance acts have provided some details about the rates, revenue administration and revenue sharing. However, still some vital issues on revenue rights are to be resolved.

Taxation powers

The taxation powers with respect to customs duty, value-added tax, excise duty, corporate income tax and individual income tax lie with the federal government, relatively these taxes are more buoyant than those assigned to the SNGs, this has created the vertical fiscal imbalance between three levels of governments. These five taxes account more than 75 per cent of the aggregate tax revenues mobilised at three levels. For example in FY 2077-78, in aggregate, the amount of revenue mobilised by three levels of governments was Rs.1151 billion, out of that, Rs.865 billion was deposited in federal consolidated fund. The taxes assigned to the SNGs, such as vehicle, land, property and entertainment taxes are less buoyant in comparison to federal taxes.

Based on the constitution, a proportion of federal government-assigned revenues are shared with SNGs, but still the bulk amount remains with the federal level. Some SNG taxes like entertainment and advertisement are reasonably buoyant, but these are not without challenges that need to be clarified about the base to be taken and rates to be defined harmoniously in horizontal levels of state units. The complaint of tax payers is that the federal government collects income tax and value added tax on these, so additional taxes on these heads at province and local level creates the space of double taxation and increases tax burden.

Other SNG taxes including agricultural income tax are surrounded by various challenges. As per the constitution, tax on agriculture income is exclusive right of province (Schedule 6). But in practice, at corporate level, this tax is collected by federal government. In reality, taxing on agriculture income at province level is not so easy. For example in India too, the states are unable to levy tax on agriculture income that comes under their jurisdiction. In case of other taxes too, like house rent tax, business tax, tourism tax, there are so many issues related to the jurisdictions, determinants of base and rates, tax administration and tax sharing, which have made the tax mobilisation scope more complicated.

Presently, on the one hand, the current expenditure of the federal government has exceeded the amount of revenues and running with revenue deficit. For example, in FY 2079/80 the amounts of revenue collected and actual recurrent expenditure are Rs.957 billion and Rs.1006 billion respectively. On the other, for the resources, the SNGs are almost dependent on the federal government since their share of own source revenue is less than one-fifth of their total expenditure. The royalties from natural resources and tourism fees do relate to the same revenue base and are listed in the concurrent list (Schedule 9). Sharing arrangement of royalties among the tiers of the governments needs to be improved.

Value added tax

As per the IGFM Act 2074, the amount of value added tax and excise duty collected from domestic products by the federal government is distributed between the federation, province and local level in ratio of 70 per cent, 15 per cent and 15 per cent respectively. The royalties from mountaineering, electricity and natural resources is also shared in ratios of 50 per cent, 25 per cent and 25 per cent basis but the IGFM itself does not explain the basis for these proportions. In regard to sharing of the royalties, as per the National Natural Resource and Fiscal Commission, in the case of local level, one of the criteria is coverage of forest. Due to these criteria, numbers of municipals are losing the amounts, since there is no forest in their location.

For the success of federalism, the functional load should be matched with the revenue assignments and resources. On the basis of mentioned provisions it is hard to achieve the goal of successful federalism. So, to resolve the issues and challenges, a comprehensive reform framework is required with incorporation of the policy, system and procedure comprising the plan of strengthening the province/local government’s accountability to the citizens that must contribute to its revenues.

Way forward

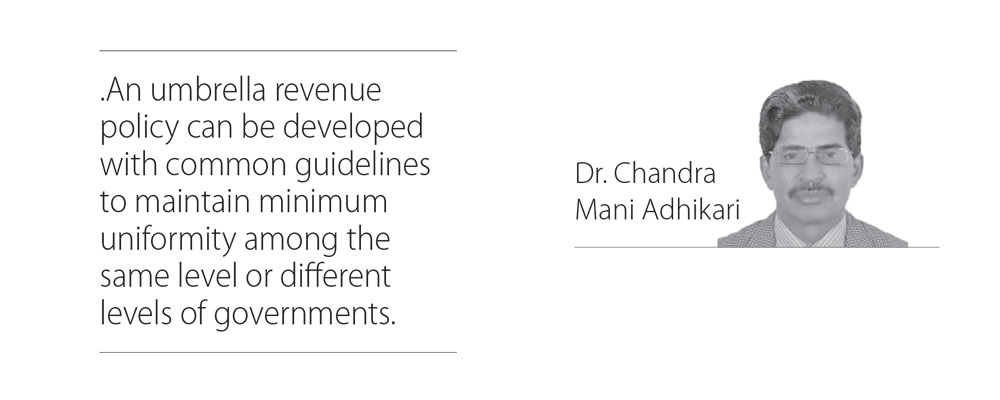

To address the challenges, the review and amendment of prevailing policies and laws is a must to ensure clarity and consistency about the revenue rights of the governments. Assisting to improve own source revenue, digitisation of revenue administration, establishing of grievance handling mechanism and identification of new sources of revenue at SNGs can be other important measures to this end. Other options include introduction of piggy-back mechanism, allocation of appropriate shares for the SNGs on federal taxes like VAT, excise, and income taxes and exploring identification of new taxes and non-tax revenues. An umbrella revenue policy can be developed with common guidelines to maintain minimum uniformity among the same level or different levels of governments. Finally, given reform measures will definitely be helpful to clarify the revenue rights and discretion of the federal government and SNGs very carefully.

(The author is an economist.)