- Sunday, 24 May 2026

Bridging Funding Gaps

Social protection systems face mounting challenges as natural hazards and climate risks increase in intensity and frequency, particularly in low- and middle-income countries. In response, many governments have introduced integrated systems designed to cushion poor and vulnerable groups against shocks, so-called adaptive social protection (ASP) systems. These are only effective if properly funded, however. In times of crisis, governments must scale up social protection budgets, with existing social protection programmes being expected to absorb additional funds and deliver relief rapidly. Yet in practice this is easier said than done.

Governments have several options to address budgetary shortfalls during disasters. For example, they can allocate funding to contingency budget lines and government reserve funds, which function like a government savings account. Historical loss and damage data indicate the amount of savings that will be required to meet emergency needs. However, when rare but severe disasters occur, governments must decide whether to reallocate funds, borrow heavily or seek ad hoc humanitarian aid from international partners. These measures involve risks such as fiscal instability, rising debt and dependence on donors.

Alternatively, pre-arranged financing can help governments scale up funding for shock-sensitive social protection systems in the event of a disaster. One increasingly common tool is climate risk insurance. Governments pay annual premiums to insurance providers and, if disaster strikes, receive payouts based on pre-agreed triggers. In 2024, for example, the government of Zimbabwe received a $ 16.8 million payout from the African Risk Capacity (ARC) Group, a regional insurance provider, after a failed agricultural season and severe food insecurity following drought.

While insurance can provide significant support, it comes with caveats: premiums are costly, and payouts are only as effective as the systems that deliver them. Without functioning distribution systems, a timely insurance payout can struggle to reach those who need it most. The growing recognition of the importance of integrating risk finance into social protection systems is reflected in a recent report and guidance commissioned by the UN Development Programme (UNDP). The guidance will be implemented across UNDP country projects where risk finance is being applied, ensuring that strengthened delivery systems complement these efforts.

The way climate risk insurance payouts are designed not only dictates who receives payments, but also how quickly and reliably funds reach those in need. There are generally two types of climate risk insurance payout: direct payouts, whereby the beneficiary receives the money directly from the insurance provider, and indirect payouts, whereby the insurance provider first transfers the payment to an intermediary agency – e.g. a government body, social protection programme or mobile banking provider – which in turn distributes the benefit directly or indirectly to the final recipients.

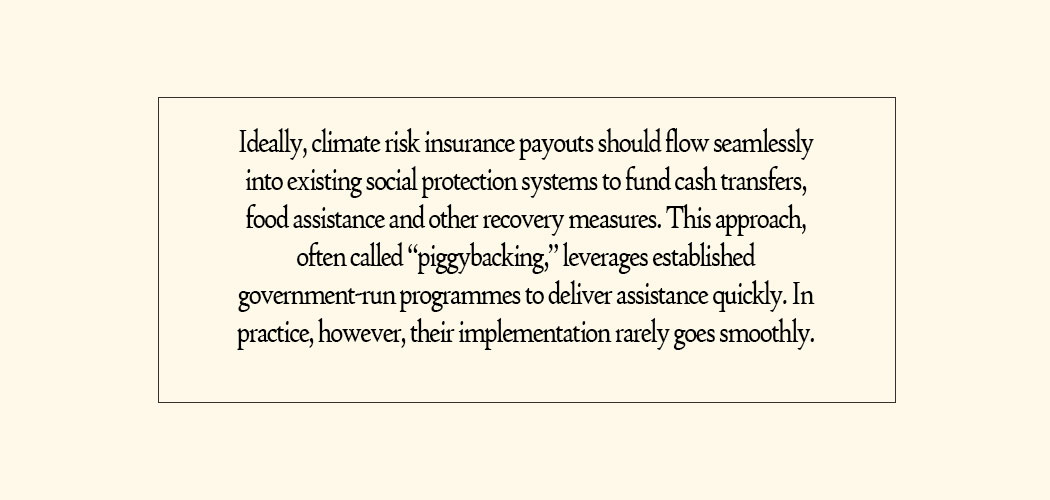

Ideally, climate risk insurance payouts should flow seamlessly into existing social protection systems to fund cash transfers, food assistance and other recovery measures. This approach, often called “piggybacking,” leverages established government-run programmes to deliver assistance quickly. In practice, however, their implementation rarely goes smoothly.

Climate risk insurance is one of several tools for pre-arranged disaster financing. Governments can also arrange emergency response funds, sovereign contingency loans and catastrophe bonds (cat bonds). Like climate risk insurance, these instruments help governments to bridge fiscal gaps when disaster strikes. They can channel funds or payouts from these instruments into adaptive social protection systems, ensuring that relief reaches the most vulnerable. But a crucial question remains: Do these mechanisms simply fill short-term funding gaps, or do they also drive sustainable poverty reduction and resilience?

-Development And Cooperation