- Thursday, 11 June 2026

Financial Literacy Aids Earning

Literacy is mostly used to understand if people can read and write or not. However, even people who may have high educational qualifications may not have various skills of leading a successful and happy life. One of them is managing one’s own finances. Financial literacy is the ability to understand and effectively use various financial skills, including personal financial management, budgeting and investing. People need to understand how whatever resources we have can be managed in such a way that we are able to make the maximum of what we have. A basic foundation and skills of developing a smart relationship with money will help individuals to understand the financial aspects throughout one’s life cycle.

During the early 2000, the Nepal Rastra Bank (NRB) conducted a research in the Terai, hill and mountainous region to understand the financial habits of people. People all over Nepal had a strong concept of saving and credit was mainly associated with taking help from relatives and the moneylenders from their community. The concept of investment and managing money was not very clear. People, mainly, in the Terai region took loan for unproductive activities like expenditure during marriage and festivals. Such expenses never earned returns to the people spending the money but rather pushed them deeper into a vicious cycle of debt and poverty.

Awareness

Since then, there have been several awareness and training to people, both from the rural and urban area and different wealth groups, on financial literacy and financial education. There have been positive changes, however, looking at the massive expenditure and gaudy marriage functions that are happening across the country indicates that more work needs to be done. Clients of the microfinance industry are now repeatedly complaining that they are being charged exorbitant interest rates. Then there are the issue of moneylenders exploiting people and taking their lands and other assets. So why are clients still taking credits from organisations charging high interest rates and why are people still taking money from moneylenders and losing their assets? This is mainly because they do not understand how to make their money earn more.

There are big holiday destination wedding ceremonies done by business tycoons and celebrities where business transactions are made that benefits the people who host them. The general people who see such weddings try copying it by taking loans and spending on extravaganza from which there is no return. In Nepal, weddings now have addition of events like haldi, sangeet and mehendi which have been infiltrated via the Bollywood movies. The Hindu weddings in Nepal had simple events like bukuwa and alta. Now both these events are arranged as separate events with different dress codes and a lot of fanfare. It is fun and frolic which cuts a dent in the pockets of who pays for it.

In Western countries, young people who plan to get married, start planning and setting aside certain amount of funds for their wedding. Such plan includes when they want to get married and in what style and also when they want to have a child. Then the couple jointly prepare a budget for these events and start saving accordingly. This is called financial planning and management. In Nepal, wedding costs are still met by parents. Most of these parents never plan on how much to spend during their children’s weddings. The traditional weddings in every culture have a set of activities fixed by the priest which has to be observed but for the add-ons like the haldi, mehendi, and sangeet in big hotels and party palaces are mostly not budgeted for.

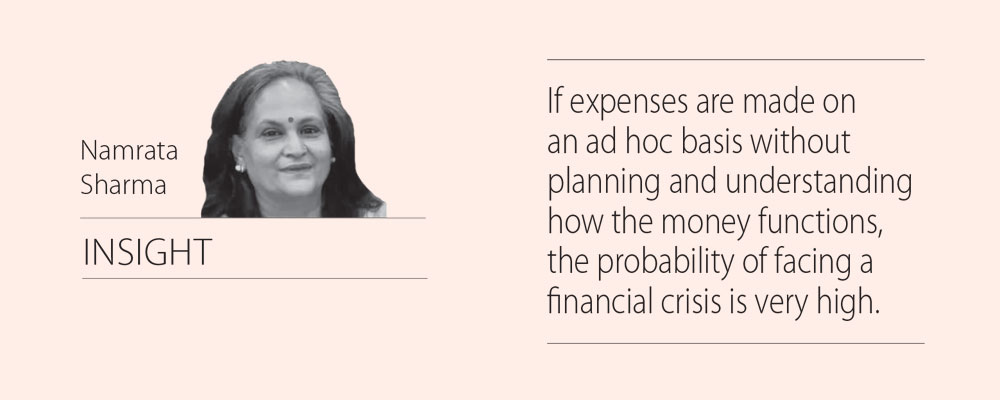

If people start saving and planning for any events whether that is productive or not, and in that planning if they built in a contingency plan to meet any risk factor that may come up, they will not have financial crisis. However, if expenses are made on an ad hoc basis without planning and understanding how the money functions, the probability of facing a financial crisis is very high. One must always remember that we need to make whatever money we have to earn more money for us. If we start spending without planning and return, the consequence could be devastating.

Clients of the microfinance industry mandatorily need to be put through training on how to understand their money and how to plan for all major investments in their life cycle, like marriage, child birth, education, land purchased and house construction, and health. There are some excellent examples of sustainable microfinance institutions in Nepal. A few savings and credit cooperatives headed by women to help each other manage their finance and also have a communal co-operation to save themselves from different forms of violence have set examples of managing their money well.

Duplication of clients

With support from outside on training and financial management, these women headed cooperatives started during the late 1990s now have hundreds of members who understand their money and have moved towards financial and economic growth. Unfortunately, it is also a reality that in Nepal, the microfinance industry has increased in such a way that there have been duplication of clients who are members of several microfinance institutions and many take loan from one to pay the interest of another. On top of that they also take loan from the local moneylenders.

Although the NRB has a policy of conducting financial literacy and education, the fact that the streets around Baluwatar are thronged by people who have faced the brunt of credit they have taken which led them to becoming landless, indicates that financial literacy and education has not been done properly and people still do not understand their money to make it earn for them rather than push them more and more into poverty.

(Sharma is a senior journalist and women rights advocate namrata1964@yahoo.com Twitter handle: @NamrataSharmaP)