Friday, 26 April, 2024

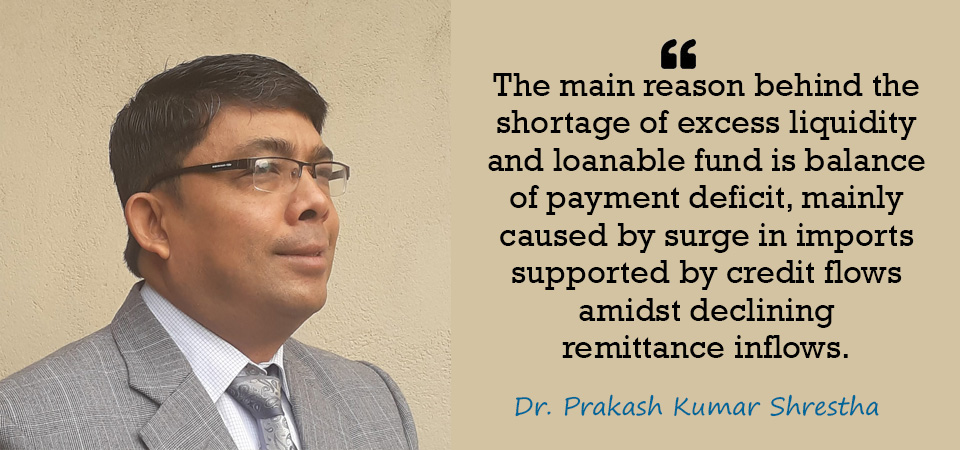

Dr. Prakash Kumar Shrestha

The Nepali banking sector, from the beginning of the second month of the current fiscal year 2021/22, has been experiencing a shortage of loanable fund. Some people even consider it as liquidity shortage. Liquidity implies the availability of cash or financial assets which can be easily converted into cash in short notice. There is no liquidity shortage for running payment systems in the economy, though. However, there is not enough excess liquidity or loanable fund for lending in the banking system in recent months.

Due to lack of enough excess liquidity, which is the cash balance held by the banks and financial institutions (BFIs) less cash reserve requirement (CRR) imposed by central bank for financial stability purpose, the short-term interest rates such as interbank rate and treasury bill rates have now reached close to five per cent. Such interest rates were below one per cent in the same time in the previous fiscal year owing to the slackness of economic activities caused by COVID-19 because of which the government imposed three months long tight lockdown and partial lockdown for another three months to restrict the contagion.

In recent months, BFIs have been heavily utilising standing liquidity facility (SLF) available from Nepal Rastra Bank (NRB). Under SLF, BFIs can borrow from NRB by pledging government securities for a week. BFIs have utilised SLF facilities of Rs. 1363 billion and overnight repo of Rs. 44.8 billion on a turnover basis as of November 10, 2021. Further, NRB has provided repo of Rs. 180 billion on a cumulative basis up to that date. BFIs have been holding more than Rs. 700 billion of government securities which can be used to borrow from NRB.

Shortage of loanable fund

Why the banking system has been facing the shortage of loanable fund? In the previous fiscal year, almost all economic activities remained close resulting in fall in both imports and credit flow. In contrary to general expectations, remittance inflows remained strong. At the same time, considering the likely contraction of economic activities, NRB followed the loose monetary policy by lowering CRR and other policy rates, and started providing more than Rs. 200 billion of refinance facilities at very concessional interest rates. Because of these reasons, the banking sector had abundant liquidity so that short-term interest rates fell below one per cent and interest rate on lending also came to a single digit.

Only after first quarter of FY 2020/21, with the gradual lifting of the restriction on various economic activities by the government and on the backdrop of easy availability of loans at low interest rates, many economic activities started recovering, stock index increasing, credit flow rising and so is the situation for imports. Despite almost lockdown like situation in the first quarter and the second lockdown imposed in the last quarter of 2020/21 because of second wave of surge in infection at a higher rate, imports and credit flows continuously went up substantially. The FY 2020/21 registered private sector credit growth of 27.3 per cent compared to just 12 per cent in the previous year. Likewise, the imports grew by 28.7 per cent in 2020/21 in contrast to a decline of 15.6 per cent in 2019/20.

Because of heavy import growth supported by credit growth, already in June 2021, balance of payments turned into negative of Rs. 15 billion in contrast to huge surplus of Rs. 282 billion at the end of 2019/20. Surge in imports kept on going during the period of second lockdown and thereafter. Hence, imports during the first three months of current fiscal year increased by 63.7 per cent, resulting in average monthly imports of Rs. 160 billion. However, remittance inflows remained stagnant in volume in the recent months, but the growth of remittance turned into negative rate of 6.3 per cent as of mid-September 2021.

On stagnant remittance inflows, the continued surge in imports has been financed by credit flows, which has increased by about 32.5 per cent in the first two months of 2021/22. However, the deposit growth remained just 21.7 per cent, which is less than the credit growth. Situation of higher credit growth compared to deposit growth still continues as of now. Credit creation also creates deposits if it is utilised domestically. In this case, increase in credit flows does not generate shortage of liquidity in the banking system. But, when credit is used for import finance, then it is the leakage of the liquidity from the system. Deficit in balance of payments is in fact a leakage of liquidity from the domestic economy. In recent months, it is happening in Nepali economy, which is the main reason for the shortage of excess liquidity as well as loanable fund in the banking system.

Though there is shortage in excess liquidity, the banking system has enough liquid assets in terms of government securities which can be used for borrowing from NRB. However, if the injection of liquidity is used for further financing imports, it will further deplete the foreign currency reserves by increasing balance of payments deficits. The availability of foreign currency reserves has already declined to cover just over seven months of imports of goods and service. Further fall in foreign exchange reserves is likely to endanger external sector stability. Hence, the main reason behind the shortage of excess liquidity and loanable fund is balance of payment deficit, mainly caused by surge in imports supported by credit flows amidst declining remittance inflows.

Remedies

Market based adjustment requires rise in interest rates to some extent. In the previous years, interest rate had declined substantially. Rise in interest rate will reduce consumption and increase savings, which is good for increasing deposit mobilisation. Moreover, increase in interest rate will make imports slightly costly because of which demand for imports will decline to some extent. Already, BFIs have raised interest rates, which is in right direction for correcting current situation.

With rise in interest rates, productive sectors, which have just started to recover from the pandemic, seem to suffer. To support these sectors, NRB can provide refinance facility selectively and BFIs should implement interest subsidy concessional lending programme of government effectively, for which government should provide enough budget for interest subsidy. In this way, some hard-hit sectors should be protected by selective interventions, and let the market do the correction in other sectors.

(Shrestha is Executive Director of Nepal Rastra Bank)

Do not make expressions casting dout on election: EC

14 Apr, 2022

CM Bhatta says may New Year 2079 BS inspire positive thinking

14 Apr, 2022

Three new cases, 44 recoveries in 24 hours

14 Apr, 2022

689 climbers of 84 teams so far acquire permits for climbing various peaks this spring season

14 Apr, 2022

How the rising cost of living crisis is impacting Nepal

14 Apr, 2022

US military confirms an interstellar meteor collided with Earth

14 Apr, 2022

Valneva Covid vaccine approved for use in UK

14 Apr, 2022

Chair Prachanda highlights need of unity among Maoist, Communist forces

14 Apr, 2022

Ranbir Kapoor and Alia Bhatt: Bollywood toasts star couple on wedding

14 Apr, 2022

President Bhandari confers decorations (Photo Feature)

14 Apr, 2022